Bangladesh’s economic outlook for August 2025 presents a mixed picture, with external stability offset by troubling weaknesses in domestic investment, revenue mobilisation and development spending, according to a government report.

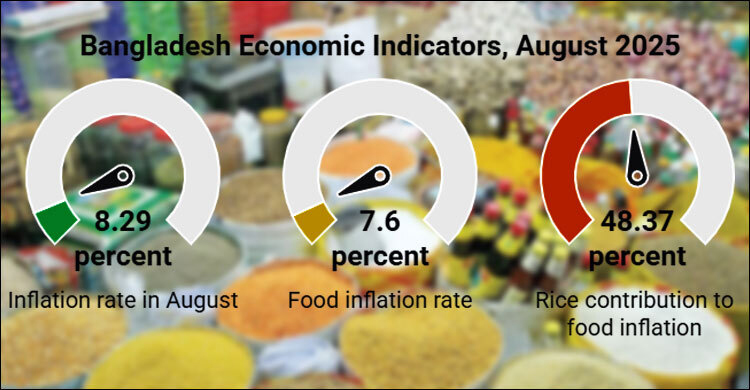

The General Economics Division (GED) of the Planning Ministry, in its latest monthly update, said inflation fell to 8.29 percent in August, the lowest since July 2022. This marked a sharp turnaround from the double-digit levels recorded between July and December 2024.

Non-food inflation dropped below 9 percent for the first time in 20 months, cushioning a slight rise in food prices. Food inflation held steady at 7.6 percent for three consecutive months, a significant drop from the 14 percent peak of July 2024.

Rice continued to drive food inflation, accounting for 48.37 percent of the basket in August. Government procurement of 1.7 million tonnes of Boro rice, duty-free imports of half a million tonnes and increased distribution under public food schemes are expected to ease price pressures. However, GED noted that delays in monitoring and policy response hindered earlier stabilisation.

External resilience

The external sector remained robust. Export earnings topped $4 billion for consecutive months, reaching $4.77 billion in July 2025. The exchange rate held steady at Tk 121–122 per US dollar, while foreign exchange reserves climbed from $24.86 billion in September 2024 to $31.17 billion in August 2025, providing what GED described as a “solid cushion” against trade shocks and debt obligations.

Domestic headwinds

By contrast, the financial sector showed deep stress. Private sector credit growth plunged to 6.49 percent in June 2025, the lowest on record and far short of Bangladesh Bank’s target. Businesses remain hesitant to borrow due to high interest rates, political uncertainty and cautious bank lending.

Public sector credit, however, rose sharply by 13.09 percent, reflecting the government’s growing reliance on bank borrowing to finance its fiscal deficit. GED warned this trend is “crowding out” private investment and threatening future job creation.

Revenue mobilisation also lagged. Collections in August stood at Tk 27,162 crore, falling Tk 3,727 crore short of target. Although receipts rose 17.6 percent year-on-year, weaker import duties and income tax collections weighed heavily. Only local VAT showed improvement. The report flagged persistent gaps as a major risk to achieving the annual revenue target of Tk 4,99,000 crore.

Development spending remained sluggish. ADP utilisation dropped to 2.39 percent of allocation during July–August FY26, down from 2.57 percent in the same period last year. August utilisation improved slightly year-on-year to 1.71 percent from 1.52 percent, but GED said such early underperformance reflects “structural bottlenecks, bureaucratic delays, and weak fund release capacity.” It warned this could result in back-loaded and inefficient spending.

Outlook

While falling inflation and rising reserves signal stabilisation, GED cautioned that domestic weaknesses threaten to erode growth momentum.

“The economy is showing resilience externally but risks remain high domestically. Without urgent measures to stimulate private credit, enhance revenue collection, and accelerate ADP implementation, medium-term growth prospects may weaken,” the report concluded.

Source: UNB